Account to Account Payments.

Banked has enabled payments to move instantly from one account to another. This means no delays as funds are never flushed through a third party.

It’s tricky to know where to start with account-to-account (A2A) payments. Mostly because it seems like, for a well rounded write-up, it should probably be with PSD2; however, it’s 2020, we’ve barely emerged from four years of every financial blog, tweet, and media outlet’s ravenous and intensely thorough coverage of the revised directive. There’s probably just enough juice for Buzzfeed to squeeze out a ‘Which PSD2 Article are you?’ quiz before the content river runs completely dry.

That said…

PSD2

It’s thanks to PSD2 that Banked, and payment initiation service providers (PISPs), can exist. PSD2, and its inherent facilitation of Open Banking, invited a revolution by opening a window into the private lives of the incumbents.

Under PSD2, banking behemoths were required to free their data, simultaneously giving the consumer greater access to information and third party providers the potential to:

A) initiate payments

B) provide consumers with a rich, consolidated view of all account activity

This was FinTech Christmas.

Open Banking brought something entirely new to the table: it championed the consumer. Previously, incumbent banks had the security blanket of widespread inertia. Banking, for the individual, was no different than paying your gas bill; it was a basic and perfunctory task.

The standard banking experience for everyone in the UK looked a bit like this:

Age 11, you apparently have a basic savings account at one of the Big Four banks — your mum has the details in a drawer somewhere

Age 17, you either:

- Keep the account your mum opened- Open an account at one of the Big Four because you’re going to uni and would like a student overdraftAge 34, you open a basic savings account at one of the Big Four for your first born

ISAs optional.

The new wave.

FinTech was erupting. This was its moment. Every challenger bank was adaptable, fresh, ready to churn out all the consumer focused app functionality seen on their public roadmaps. The incumbents, embroiled in systemic bureaucracy and archaic infrastructure, weren’t as nimble. This was the first time traditional banking had been been threatened.

However, the incumbents had decades of trust where the challengers were unknowns, and challengers also had the job of educating consumers (the majority of whom probably, understandably, didn’t have a natural proclivity towards financial content). This slow, laborious, and fragile process of building trust alongside a national education added a time sensitive element to challenger success — who can do it first, best, and before the incumbents catch up?

However, as interesting as it is to watch unfold, Banked doesn’t have a horse in this race.

At Banked, there is one pertinent rule: if the consumer is happy and secure with their banking allegiance, then that’s a bank we’re glad to support. Banked is connected to all major UK banks, and constantly working on expanding this network, with a view to emerge into other European territories.

So, how does Banked work with banks in this new, PSD2 illuminated world?

Account-to-account payments.

Here she is, what we’ve all been waiting for: A2A.

As discussed above, prior to PSD2, there had been an inertia in banking technology and infrastructure. This includes the ‘payment rails’ along which transactions move. These payment rails were created decades ago and have remained unchanged. Banked has developed an alternative set of rails, rails created for the digital age, rails which enable real-time, account-to-account payments.

So, what are account-to-account payments? They’re just that. Sounds underwhelming, doesn’t it? And here’s where PISPs hit a similar problem to the challengers: education. Only the PISP struggle has an extra layer of complexity, as it’s (logically) assumed that account-to-account payments are the norm. There’s nowhere else for money to go, right? Well, that’s where we need to assess how we imagine credit and debit cards.

Typically, cards are interpreted as the physical manifestation of an account. It’s the tangible to the digital. And whilst this isn’t conceptually inaccurate when applied to function, it’s inaccurate when applied to process.

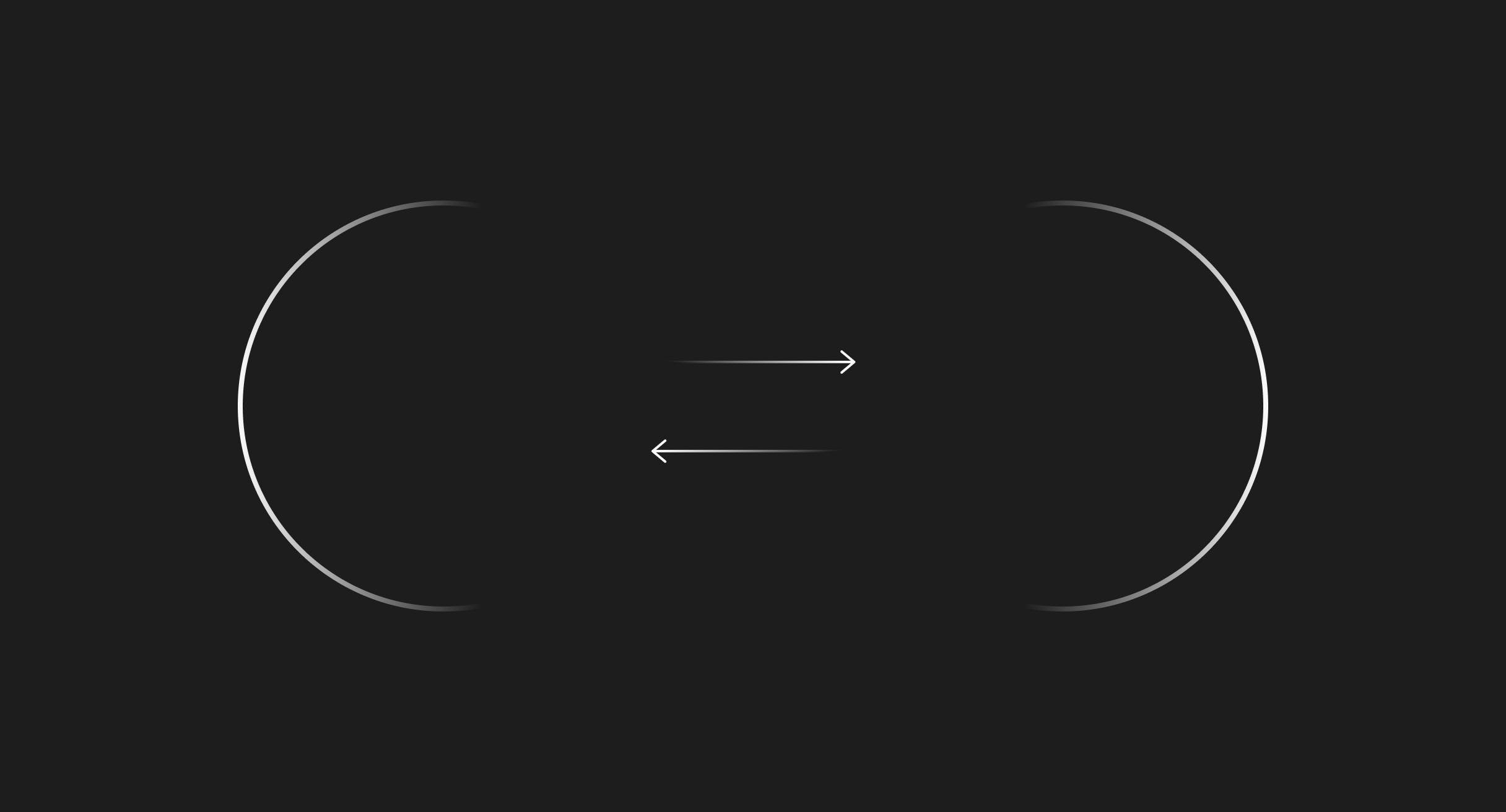

Imagine instead:

Your card is a destination. A stop. A detour on the journey from A to C.

Probably difficult to imagine without this image.

So far, B (your card) has been a necessary step in payment flows; however, depending on what card you use, B could both delay the payment and charge (the merchant) for the inconvenience.

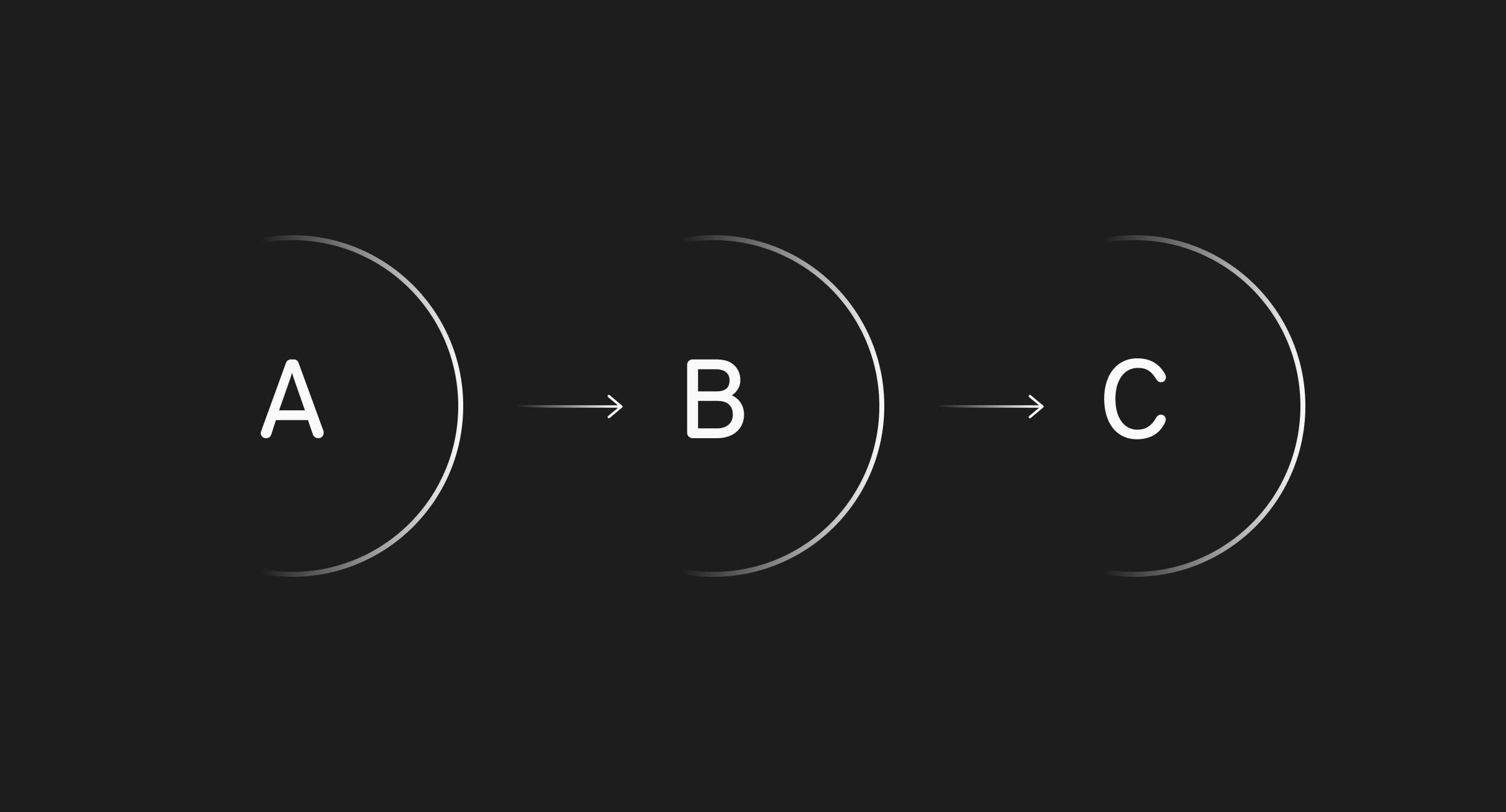

When reworking the rails, Banked removed that pesky B:

Look at those more efficient circles.

Using data freed during PSD2, Banked has enabled payments to move instantly from one account to another. This means no delays as funds are never flushed through a third party, Banked simply facilitates the connection and the consumer can securely approve the payment from within their banking app.

Here, we see an interesting change in mechanics around push vs. pull. The card system takes (pulls) money from your account, whereas account-to-account asks you to approve (push) the payment.

Additionally, the speed and inherently lean nature of this new digital payments infrastructure means Banked can pass benefits on to merchants: costs are over 99% lower than standard payment processing fees, potentially saving e-commerce giants £100,000s per year; Banked’s flat fee structure helps support tiny businesses by removing the high fee percentage associated with small transactions; and the instant nature of A2A frees fledgeling start-ups from the concerns of delayed payments.

Moreover, account-to-account removes friction from the emerging world of social payments. A little something we’ve got our eye on.

Platform

Legal

52 Lime Street, London, England, EC3M 7AF

Company number 11047186 : Firm Reference Number 816944 : +44 (0) 20 8090 2747

© Banked : 2026